Received 19 February 2022; Revised 21 May 2022; Accepted 8 June 2022.

This is an open access paper under the CC BY license (https://creativecommons.org/licenses/by/4.0/legalcode).

Safi Ullah Khan, Ph.D., Senior Assistant Professor, UTB School of Business, Universiti Teknologi Brunei, Jalan Tungku Link Gadong BE1410, Brunei Darussalam, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

Abstract

PURPOSE: We examine whether financial obstacles affect the probability of a firm undertaking previously suspended (or abandoned) innovation projects for new product development (NPD), and whether extramural R&D, as well as the breadth of the types of R&D collaboration (i.e., knowledge sources), moderate the relationship between financing constraints and the probability of restarting previously suspended NPD from selected South Asian economies. METHODOLOGY: This study controls for potential endogeneity in innovation propensity and finance access by employing a recursive bivariate probit model. We also adopt an instrumental variable approach by employing a probit model with continuous endogenous regressor to account for the potential endogeneity between the breadth of collaboration partners and innovation propensity. FINDINGS: Financial obstacles significantly impact previously suspended NPD. Furthermore, extramural R&D positively affects the probability of a firm undertaking NPD projects and attenuates the relationship between financing constraints and the likelihood of restarting abandoned/suspended NPD projects, suggesting that extramural R&D alleviates financing constraints, which increases the likelihood of NPD restarts. However, the breadth of collaborating partners is not positively associated with the probability of a firm restarting NPD. This is consistent with the view that extramural R&D with diverse sets of partners is exposed to the risks of the “two worlds paradox” arising from a firm’s collaboration with universities, research institutions, and consulting firms. IMPLICATIONS: The findings corroborate the view that firms must maintain a balance between their internal knowledge base and extramural R&D to optimize innovation outcomes. Nevertheless, extramural R&D reduces the reliance of financially constrained firms on resource requirements, improves access to financing, and enhances R&D productivity in NPD. ORIGINALITY AND VALUE: We provide the first firm-level and multi-country evidence of the importance of financial obstacles in the probability of reinitiating previously suspended NPD at the execution phase. Second, to the best of our knowledge, this is the first study to examine the relationship between inter-organizational R&D collaboration diversity and the probability of a firm reinitiating previously abandoned (or suspended) NPD.

Keywords: New Product Development, financial constraints, extramural R&D, inter-organizational R&D collaborations, external knowledge acquisition

INTRODUCTION

Technological innovation is vital to a firm’s innovation performance and success (Rauter, Globocnik, Perl-Vorbach, & Baumgartner, 2019). However, many innovation projects fail (or are abandoned) before their successful conclusion because several contingencies affect innovation performance, such as temporal coordination constraints, failure of innovation systems (Greco et al., 2020), and whether their suspension is an outcome of a lack of financial resources or intangible organizational competencies, knowledge, and capabilities (Hewitt-Dundas, 2006). These resources may be found beyond a firm’s boundaries by leveraging its in-house R&D through extramural (i.e., collaborative) R&D, which can help the focal firm exploit externally acquired knowledge, sustain innovation (Santamaría, Nieto, & Rodríguez, 2021), and improve the likelihood of reinitiation of previously abandoned (or suspended) projects for new product development (NPD). This study examines whether extramural R&D affects the likelihood of a firm restarting innovation activities for NPDs that have been suspended or abandoned before completion.

The extant literature has acknowledged the relevance of financial obstacles to technological innovation (Canepa & Stoneman, 2008; Howell, 2016; Peng, Tan, & Zhang, 2020). Financial constraints prevent many firms from completing innovation activities, and may negatively affect the likelihood of restarting abandoned innovation projects for NPD. Mohnen et al. (2008) and Garcia-Vega and Lopez (2010) found that financial obstacles significantly affect the probability of premature stopping, abandoning, or not starting NPD innovation projects. Furthermore, because market friction is more severe in developing markets, financial constraints are likely to affect R&D investments and their eventual success or failure (Sasidharan, Lukose, & Komera, 2015). Our second main research objective is to examine whether extramural R&D and breadth in the types of R&D collaboration (i.e., open innovation sources) moderate the relationship between financing constraints and the probability of reinitiating previously abandoned (or suspended) NPDs.

This study contributes to the literature on corporate innovation in three ways. First, previous studies examined how R&D collaborations overcome the contextual causes of innovation failures, suspensions, and abandonment (Antonioli, Marzucchi, & Savona, 2017; Radas & Bozic, 2012). Greco et al. (2020) show that firms collaborating with an extensive network of partners are less likely to abandon innovation activities. Recently, González-Moreno et al. (2019) showed that “coordination difficulties and bounded rationality” explain the inverted U-shaped relationship between breadth of knowledge sourcing and innovation propensity. Loss of control over critical internal know-how, increased managerial and/or organizational complexity, and the consequent increased costs (Gkypali, Filiou, & Tsekouras, 2017) associated with accessing a diverse set of knowledge from different collaborating partners may outweigh the positive effects on a firm’s internal innovation outcomes. To the best of our knowledge, ours is the first study to examine the relationship between diversity in R&D collaboration and the probability of a firm reinitiating a previously abandoned (or suspended) NPD. We found that firms collaborating with a broader network of partners, such as domestic and foreign firms, academic institutes, and research organizations, are less likely to restart or attempt to start previously abandoned NPD projects. This result corroborates the “two-worlds paradox” (Hewitt-Dundas et al., 2019) arising from R&D collaborations between firms and academic research institutes. Our results imply that the innovation propensity concerning the reinitiation of previously suspended NPD benefits from a firm’s extramural R&D, consistent with the idea that firms gain substantially from extramural innovation investments (Wadhwa, Bodas Freitas, & Sarkar, 2017). However, collaborating with a diverse set of partners also increases certain costs (e.g., transaction costs, managerial attention constraints, and coordination costs), which may hamper firms’ propensity to restart previously suspended NPDs.

Second, we provide the first multicountry evidence from three South Asian countries on the importance of financial obstacles in the probability of initiating or attempting to develop an innovative product and service at the execution phase. For the empirical analysis, we used a unique enterprise innovation survey conducted as a follow-up to the baseline enterprise surveys by the World Bank Group in South Asian countries in 2013 (India, Pakistan, and Bangladesh) which collected detailed firm-level information on various types of innovation and innovation-related activities. Pakistan, India, and Bangladesh are major representatives of South Asia and relatively understudied in the literature on the interaction between financial obstacles to innovation and extramural R&D. Although they are neighboring countries with close geographical proximity and many similarities in terms of culture, religion, and shared history, they also differ in their level of economic development, financial market development, access to external financing, and corporate innovation. India’s economic growth over the last few decades has mainly been attributed to advances in manufacturing-led development and corporate innovation. Asian economies, particularly India, have invested massively in transforming into a knowledge economy and private firms have shown increased innovation performance (Zhang, Zhao, Voss, & Zhu, 2016). Empirical evidence on innovation propensity for NPD in the South Asian context is also much needed because corporate expenditure on R&D in developing countries such as India has increased exponentially over the last decade (Ivus, Jose, & Sharma, 2021), some of which is attributed to increased product-market competition following the abolition of License Raj (Bas & Paunov, 2018) and the strengthening of the intellectual property rights regime (Dhanora, Sharma, & Khachoo, 2018). By contrast, South Asian countries appear to be laggard in improving the corporate R&D environment because R&D expenditures (as a percentage of GDP) for India (0.50% in 2018) and Pakistan (0.24% in 2017) are much lower than the world’s average expenditure of 2.2% in 2018 (World Bank, 2021). However, with the opening up of the Indian economy to international trade and investment in the 1990s, after decades of excessive banking regulations and illiquidity of capital markets and the gradual shift towards R&D and industrialization policy goals and innovation, Indian enterprises have progressed in technological innovation (Altenburg, Schmitz, & Stamm, 2008). India has one of the more developed capital markets and modern financial systems among developing countries (Allen, Chakrabarti, Qian, & Qian, 2012), but also has weak legal institutional settings and investor protections, which makes it an interesting case to examine the finance-innovation nexus in the context of developing markets. Furthermore, the absence of empirical studies on the role of extramural R&D in attenuating firm-level financing constraints on innovation propensity in South Asian economies, such as India, Pakistan, and Bangladesh, was one of the main motivating factors for the current study.

Controlling for potential endogeneity between financing constraints and innovation propensity, we show that credit constraints negatively influence the likelihood of restarting previously suspended NPDs. This result is consistent with the view that well-functioning capital markets promote technological innovation and reconcile the seemingly skeptical view of banks’ role in facilitating innovation (e.g., Amore, Schneider, & Žaldokas, 2013; Khan, Shah, & Rizwan, 2021). We also observe a preference for internal funds to finance R&D investments in South Asian countries, consistent with pecking order theory in firms’ preferences for financing innovation (Alam, Uddin, & Yazdifar, 2019). Consequently, when adequate internal funds are available, firms may undertake innovation activities such as those previously suspended or abandoned. This resumption of NPDs may be hampered if the firm is required to access external capital, which may be costly or unavailable for funding innovation.

Third, we contribute to the open innovation literature by examining whether extramural R&D moderates the relationship between financial obstacles and innovation propensity. We demonstrated that firms with extramural R&D are more likely to restart previously abandoned NPDs. Furthermore, we find that credit constraints are less binding for firms with extramural R&D, consistent with the view that R&D collaborations can produce “cost and risk-sharing” opportunities that lead to a reduction in the cost of external finance. Finally, previous studies on innovation failures and financial constraints have primarily employed self-perceived and self-reported measures of financial obstacles (e.g., Antonioli et al., 2017; García-Quevedo, Segarra-Blasco, & Teruel, 2018). We complement these studies using a direct measure of credit constraints faced by firms by utilizing loan application data from enterprise surveys. This study is similar to Czarnitzki and Hottenrott (2017), who examine whether R&D collaborations attenuates the firm’s financial constraints to innovation using the OECD R&D Survey data. They employed the sensitivity of R&D expenditures to the availability of internal funds for working capital financing as an indirect proxy for financial constraints. In contrast, we employ a direct proxy for financial obstacles using the firm’s actual experience of accessing credit markets.

The rest of the paper is organized as follows. The next section discusses theoretical background and hypotheses development. Then detailed methodology and data description are presented, followed by econometric analysis in the Empirical Results section, while the last section concludes the paper.

THEORY AND HYPOTHESES

Financing constraints and extramural R&D

Given the increasing technological complexity and multidisciplinarity of R&D activities in recent years, rapidly expanding knowledge bases have necessitated a move towards open innovation and technology partnerships (Kafouros, Love, Ganotakis, & Konara, 2020). While the relevance of R&D collaborations in exploiting externally acquired knowledge for innovation performance has been well documented (e.g., Beneito, 2006; Medda, 2018), collaborative R&D as an attenuation strategy to alleviate financial constraints has not received much attention in the literature. Antonioli et al. (2017) find that perceived financial barriers to innovation are associated with the adoption of collaborative strategies: firms resort to cooperation driven by risk and cost-sharing incentives. Similarly, Czarnitzki and Hottenrott (2017) show that financial constraints are stronger for non-collaborating firms than for other firms. Lerner, Shane, and Tsai (2003) find that when public market financing opportunities are limited, small U.S. biotechnology firms finance their R&D activities through alliances with larger corporations. Similarly, Park, Chen, and Gallagher (2002) showed that resource-poor firms are more likely to form alliances to access external resources. Alam et al. (2019) show that firms with extramural R&D utilize both internal and external financing to fund innovation, whereas firms with in-house R&D lack access to external financing for R&D investments. Piga and Atzeni (2007) documented similar findings that firms with extramural R&D are more likely to have loan applications approved by their banks. We expect firms with R&D collaborations to be less likely to depend on internal funds to undertake previous NPD projects. Hence, we propose the following hypothesis.

H1: Extramural R&D alleviates the negative effects of credit constraints

on the likelihood of restarting previously suspended (or abandoned)

NPD projects.

Inter-organizational R&D collaboration breadth and innovation

The literature on innovation management suggests that a complex, uncertain, and troubled path towards successful innovation can lead to numerous obstacles to innovation. Exogenous obstacles may be related to the failure of R&D cooperation with important external partners (Greco et al., 2020). Endogenous causes of innovation failure are related to a firm’s internal deficiencies (e.g., the focal firm’s lack of attention, required expertise and knowledge, or process inadequacies). Prior studies have documented the benefits of R&D collaboration to the focal firm stemming from the exploitation of complementary assets and capabilities and additional opportunities for mutual learning, leading to higher innovation and commercialization capabilities for collaborating firms (Koch & Windsperger, 2017). Although the benefits of extramural R&D to the focal firm have been extensively examined, no previous study has examined the breadth of collaboration and a firm’s propensity to restart innovation projects for previously suspended (or abandoned) NPDs. Firms can overcome endogenous and contextual causes of innovation abandonment by collaborating with a wide range of partners (Lasagni, 2012). Owing to their exposure to diverse sources of knowledge, firms gain new perspectives that can help them avoid cognitive myopia (Prahalad & Bettis, 1986), act as stimuli to engage in creative thinking, and identify new problem-solving approaches that may foster their propensity to evaluate and restart abandoned (or suspended) NPD projects. Thus, we propose the following hypothesis.

H2a: The higher the breadth of R&D collaborations, the higher the

probability that a firm restarts previously suspended (or abandoned)

NPD projects.

Previous studies have provided evidence of excessive costs associated with extramural R&D. Leiponen and Helfat (2010, p. 226) argues that firms “… may encounter higher marginal costs due to the increased complexity of managing both the variety of knowledge and the relationships needed to maintain access to these sources.” Gkypali et al. (2017) argue that such costs exist because there are highly interactive and complex processes between the point when external knowledge sources are accessed and the point at which knowledge is internalized and converted into tangible innovation outcomes by embedding it into organizational culture, processes, and routines. Laursen and Salter (2006) conceptualize three inter-related risks of “over-search” namely “the absorptive capacity problem, the attention allocation problem, and the not-invented-here syndrome,” which potentially can outweigh the benefits emanating from breadth in the external knowledge search. Managing multiple external knowledge sources is challenging, and many firms may not have developed the requisite managerial capabilities and organizational processes to benefit from external knowledge. Hence, innovation processes and costs associated with the breadth of knowledge sources may coexist and jointly affect NPD projects. We propose the following hypothesis:

H2b: The higher the breadth in types of inter-organizational R&D

collaborations, the lower is the probability that a firm restarts

previously suspended NPDs.

METHODOLOGY

Financial obstacles and innovation propensity may be endogenously determined. This endogeneity may arise because, firstly, innovation requires additional funding from external financiers, which may increase the likelihood of a firm experiencing financial constraints. Second, the firm’s decision to restart previously abandoned NPDs and how these innovation investments are financed may be simultaneously determined. We control for potential endogeneity between innovation propensity and the probability that a firm will face financial obstacles in funding innovation as simultaneous questions in the bivariate probit model. A bivariate model is applicable “where there are good a priori reasons to consider a dependent binary variable as simultaneously determined with a dichotomous regressor” (Monfardini & Radice, 2008, p. 271) As in García-Quevedo et al. (2018), we use recursive bivariate probit model given as follows.

(1)

(1)

(2)

(2)

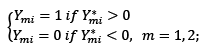

with  is determined according to the rule:

is determined according to the rule:

where  and

and  are latent variables,

are latent variables, and

and  are indicator variables: (a) firm restarts previously abandoned (or suspended) NPDs (innovation), and (b) a firm is credit-constrained (financing constraints) as defined in the Variable measurements section.

are indicator variables: (a) firm restarts previously abandoned (or suspended) NPDs (innovation), and (b) a firm is credit-constrained (financing constraints) as defined in the Variable measurements section. andare iid errors with bivariate normal distribution having variance equal to 1 and

andare iid errors with bivariate normal distribution having variance equal to 1 and . If

. If  are assumed to be uncorrelated, confirming the exogeneity assumption for the two equations, which can then be computed as independent univariate probit models. By contrast,

are assumed to be uncorrelated, confirming the exogeneity assumption for the two equations, which can then be computed as independent univariate probit models. By contrast, indicates the presenece of endogenity and requires the estimation of the two equations simultaneously to obtain consistent estimates of the two models. Following Savignoc (2008), we set

indicates the presenece of endogenity and requires the estimation of the two equations simultaneously to obtain consistent estimates of the two models. Following Savignoc (2008), we set to allow the model to be consistent in empirical estimations.

to allow the model to be consistent in empirical estimations.

Furthermore, in equations (1) and (2) is a set of controls as determinants of innovation, FC is a measure of credit constraints,

in equations (1) and (2) is a set of controls as determinants of innovation, FC is a measure of credit constraints, are country and industry fixed effects, and

are country and industry fixed effects, and  is a vector of four variables as exclusion restriction to serve as instrumental variables in equation (2). Two dummy variables for whether (a) a firm’s financial statements are audited by an external auditor, and (b) a firm has pre-existing loans and/or a credit line facility from a bank. These variables account for information asymmetry and credit worthiness and are likely to reduce a firm’s credit constraints. Third, geographical location, whether the firm is located in a main business city or capital of a country, affects access to external financing. Arena and Dewally (2012) find that rural and small-city firms face higher debt costs, consistent with the proximity hypothesis, as firms located in small and less-developed areas face informational disadvantages relative to firms located in major cities and financial hubs. Fourth, LFA is a binary variable equal to 1 if a firm has leased fixed assets. These four dummy variables are expected to affect credit constraints but are not not directly related to the firm’s innovation propsensity for NPDs. Moreover, in equation (2)

is a vector of four variables as exclusion restriction to serve as instrumental variables in equation (2). Two dummy variables for whether (a) a firm’s financial statements are audited by an external auditor, and (b) a firm has pre-existing loans and/or a credit line facility from a bank. These variables account for information asymmetry and credit worthiness and are likely to reduce a firm’s credit constraints. Third, geographical location, whether the firm is located in a main business city or capital of a country, affects access to external financing. Arena and Dewally (2012) find that rural and small-city firms face higher debt costs, consistent with the proximity hypothesis, as firms located in small and less-developed areas face informational disadvantages relative to firms located in major cities and financial hubs. Fourth, LFA is a binary variable equal to 1 if a firm has leased fixed assets. These four dummy variables are expected to affect credit constraints but are not not directly related to the firm’s innovation propsensity for NPDs. Moreover, in equation (2)  is the same set of controls as described in equation (1).

is the same set of controls as described in equation (1).

Data description

We use survey data from the World Bank Group’s firm-level enterprise surveys (ES). The ES is a rich, multi-topic enterprise-level survey that collects data on firm characteristics, financial information, the firm’s experiences in interacting with the business, legal, economic and regulatory environments. ES employs a uniform methodology across all countries, using a common questionnaire. Stratification of sample firms based on size, industries, and within-country regions make it a nationally representative sample of the country’s private sector businesses, whereas the use of standardized global methodology and master questionnaire allows comparisons of the collected data and indicators consistent across countries. The ES surveys are completed across countries through intensive face-to-face interviews with business owners and managers. In 2013, the World Bank Group implemented a separate innovation follow-up survey (IFS) in nine developing countries (four South Asian and five East African economies). The IFS revisited the same sample of firms interviewed during the standard ES surveys in these nine countries in 2013, to collect firm-level data on various types of innovation and innovation-related activities and determinants of innovation. The IFS survey is cross-sectional covering a nationally representative sample of firms from manufacturing and services sectors. The IFS survey collected firm-level data on radical and incremental technological innovations (product or service innovation and process innovation) and non-technological innovations, such as managerial-organizational and marketing innovations, and how these innovations were funded from internal and external sources of finance. The IFS also collected firm-level information on innovation-related activities such as in-house R&D and their funding sources, R&D collaborations with universities, research institutions, domestic and foreign companies, and private individuals and consultants, and the use of Information and Communications Technology (ICT). Data from the World Bank Group’s Enternprise Analysis Unit shows that some firms from the baseline ES surveys missed the completion of the innovation follow-up surveys. We merge this dataset with the baseline ES dataset using a unique firm identification code “idstd” for the three South Asian countries, namely Pakistan, India, and Bangladesh, comprising 5178 common firms from manufacturing industries and business services in the two survey data sets for the three countries, namely 990 firms from Bangladesh, 3492 from India and 696 from Pakistan.

Variable measurements

The dependent variable, PABN, captures whether a firm has attempted to restart its previously suspended or abandoned NPD innovation projects. We construct PABN from the following IFS question: “In the last three years, did this establishment attempt to develop an innovative product or service that was abandoned or suspended before completion? Yes/No”. PABN takes a value of 1 if the firm responded affirmatively and 0 otherwise.

We employ a set of explanatory variables extracted from the innovation literature. Their explanations are as follows: Knott and Vieregger (2020) find robust evidence that R&D spending and innovation increase with firm size. Large firms may overcome obstacles to innovation abandonment owing to better access to external knowledge sources (Veugelers & Cassiman, 1999). However, organizational inertia associated mainly with large firms may hamper their innovation proprensity (Coad, Segarra, & Teruel, 2016; Shah, Shah, & Khan, 2017). Group-affiliated firms benefit from within-group R&D spillovers and shared resources to sustain their innovation activities (Abdullah, Shah, & Khan, 2012). We capture a firm’s group affiliation using the dummy variable GPD.

R&D intensity (the ratio of R&D expenditure to sales) accounts for innovation effort and absorptive capacity to restart innovation projects (González-Moreno et al., 2019). This study also controls for potential complementarities between different innovation outcomes by including a dummy variable, MOI, indicating whether a firm has introduced organizational and/or marketing innovations. Skilled and qualified human capital is critical for successful innovation (Wang, Yeung, & Zhang, 2011). We construct a dummy variable, TRGI, indicating whether a firm has formal innovation-related employee training programs.

Previous research (e.g., Mateut, 2018) shows a positive link between public subsidies and increased firm-level innovation. We include a dummy variable, GNFIN, for whether a firm has received non-financial assistance from government support programs (e.g., training in the use of R&D-related equipment, NPDs, and their marketing). We also control for a firm’s ability to employ various formal mechanisms for appropriating returns to innovation. Formal intellectual property (IP) protection mechanisms – a proxy for innovation capital – foster innovation outcomes and productivity (Cohen, Nelson, & Walsh, 2002). Hall and Sena (2017), using data from three waves of the UK Community Innovation Surveys (CIS 3-5), the document that firms with more formal mechanisms of IP protection are more innovative than firms that prefer informal mechanisms of IP protection. As in Griffith, Huergo, Mairesse, and Peters (2006), we define a dummy variable, APPLY_PATENT, equal to one if a firm used at least one of the following formal mechanisms of IP protections namely “patent(s), utility model, industrial design, trademark, or copyright” to protect inventions; otherwise it takes the value 0. We constructed a binary variable, COOP, which takes the value of one if a firm has engaged in collaborative R&D for NPD with at least one of the following partners: domestic and/or foreign firms, academic or research institutes, private consulting firm, individuals, or a government agency; COOP otherwise equals 0.

As in Khan, Khan, and Ullah (2021), we construct a direct indicator of credit constraints using information from the ES survey. The firms were asked to report information on their bank loan applications, if any, submitted during the past year. The responses of loan-applicant firms were: (i) approved in full, (ii) accepted partially, (iii) rejected, and (iiv) still in process. The non-applicant firms were further required to identify the main reason why they did not apply for a loan from the following list: “(a) having sufficient funds, (b) high interest rate, (c) complex application procedure, (d) high collateral requirements, (e) mismatch of loan size and maturity, and (f) a firm’s perception that it will not get the loan”. We use these responses to construct a measure of credit constraints denoted by FC. As in Berkowitz and White (2004), Khan (2022), FC is an indicator variable that equals 1 if a firm’s loan application was rejected or accepted partially; FC also equals 1 if a non-applicant firm’s response was either b, c, d, e, or f. FC is equal to 0 if the firm’s loan applicantion was accepted in full or the non-applicant firm’s response was “(a): have sufficient funds”. Hence, FC is coded 1 for credit–constrained firms and 0 for other firms.

Descriptive statistics

Table 1 presents summary statistics of the share of credit-constrained firms, NPD restarting firms, and innovative firms (i.e., applied for patents in the last three years covered by the survey) across sectors, firm size, and countries. There is a substantial variation in the share of NPD-restarting firms across industries. Unsurprisingly, high-technology sectors, such as information technology and related services (27.9%), electronics and communication equipment (18.3%), and fabricated metal products (21.7%) had the highest share of NPD-restart firms, whereas low-tech sectors, such as furniture (3.6%), transport and storage (2.7%), and garments (9%) had lower proportions of NPD-restart firms. We observe a similar distribution of the proportion of innovative firms (i.e., those that applied for patents) across sectors, where high-tech sectors have the highest proportion of innovative firms, whereas the least innovative firms are in the low-tech sector. By contrast, we observe a fairly even distribution of credit-constrained firms across sectors, although, as expected, high-tech sectors have a slightly higher share of credit-constrained firms (i.e., 52.10%) relative to the average share of credit-constrained firms (47.4%) across the sample.

Table 1. Descriptive statistics

|

|

Restarts NPD |

|

Credit-constrained firms |

|

Applied for a patent |

|||

|

N |

Mean |

N |

Mean |

N |

Mean |

|||

|

Basic Metals & Metal Products |

227 |

18.5% |

213 |

51.6% |

229 |

47.2% |

||

|

Chemicals & Chemical Products |

388 |

10.6% |

345 |

42.9% |

388 |

42.8% |

||

|

Construction |

111 |

18.0% |

106 |

51.9% |

111 |

40.5% |

||

|

Electronics & Communications Equip. |

241 |

18.3% |

207 |

52.2% |

243 |

49.4% |

||

|

Fabricated Metal Products |

226 |

21.7% |

214 |

54.7% |

225 |

44.9% |

||

|

Food |

461 |

11.7% |

427 |

42.2% |

456 |

28.5% |

||

|

Furniture |

55 |

3.6% |

53 |

49.1% |

55 |

20.0% |

||

|

Garments |

155 |

9.0% |

140 |

26.4% |

155 |

23.9% |

||

|

Hotels & Restaurants |

147 |

15.6% |

132 |

41.7% |

148 |

28.4% |

||

|

Information Technology (IT) & IT Services |

86 |

27.9% |

85 |

58.8% |

90 |

45.6% |

||

|

Leather Products |

98 |

9.2% |

89 |

39.3% |

98 |

16.3% |

||

|

Machinery & Equipment |

282 |

17.4% |

263 |

44.9% |

281 |

38.8% |

||

|

Motor Vehicles |

253 |

12.65% |

229 |

51.5% |

217 |

43.9% |

||

|

Non-Metallic Mineral Products |

249 |

12.9% |

223 |

62.8% |

248 |

35.9% |

||

|

Other Manufacturing |

909 |

14.1% |

849 |

46.6% |

914 |

29.1% |

||

|

Other Services |

140 |

5.7% |

115 |

31.3% |

139 |

4.3% |

||

|

Rubber & Plastics Products |

276 |

14.5% |

254 |

58.7% |

275 |

45.5% |

||

|

Services of Motor Vehicles |

104 |

17.3% |

88 |

58.0% |

102 |

37.3% |

||

|

Textiles |

276 |

14.1% |

239 |

43.1% |

281 |

33.1% |

||

|

Transport, Storage, & Communications |

114 |

2.6% |

103 |

44.7% |

115 |

18.3% |

||

|

Wholesale & Retail |

322 |

13.4% |

296 |

45.9% |

296 |

19.9% |

||

|

High-Tech sectors |

2,228 |

15.84% |

2,033 |

52.10% |

2,234 |

43.47% |

||

|

Total (whole sample) |

5120 |

13.9% |

4670 |

47.4% |

5132 |

33.8% |

||

|

Panel B: Stratification by firm size |

||||||||

|

Small firms (< 19 employees) |

1473 |

12.9% |

1379 |

49.4% |

1472 |

23.8% |

||

|

Medium-sized firms (20 – 99 employees) |

2214 |

15.0% |

2011 |

50.2% |

2217 |

36.6% |

||

|

Large firms (100+ employees) |

1433 |

13.5% |

1280 |

41.0% |

1443 |

39.8% |

||

|

Panel C: Country-wise stratification |

||||||||

|

India |

3446 |

17.5% |

3195 |

51.9% |

3457 |

39.9% |

||

|

Pakistan |

685 |

5.0% |

542 |

34.7% |

686 |

14.9% |

||

|

Bangladesh |

989 |

7.7% |

933 |

39.7% |

989 |

25.5% |

||

|

Panel D: NPD project reinitiation and credit constrained firms |

||||||||

|

N |

Credit-constrained firms |

|||||||

|

NPD restart firms |

714 (14%) |

301 (42%) |

||||||

|

NPD non restart firms |

4,406 (86%) |

53% |

||||||

|

Share of firms restarted NPDs |

||||||||

|

Credit-unconstrained firms |

13.7%* |

|||||||

|

Credit-constrained firms |

15.2% |

|||||||

Note: This table presents the descriptive statistics for the proportion of credit-constrained firms, NPD restart firms and innovative firms across sectors, firm sizes, and countries. High-Tech sectors refer to technology-intensive industries namely ‘chemicals, electronics & communications, engineering, rubber & plastics, Information Technology and related services.”

Interestingly, the distribution of NPD-restart firms is fairly even across firm sizes (Panel B, Table 1), whereas smaller and medium-sized enterprises are more credit-constrained than larger firms, and larger firms have the highest share of innovative firms (applied for patents). As expected, the country-wise distribution of the sample shows that India has a significantly higher proportion of NPD-restart (17.5%). This is also supported by the accompanying statistics for innovating firms as India has the highest share of innovative firms (39.9%) than Pakistan and Bangladesh do. However, India has the highest proportion of credit-constrained firms relative to the other two countries. Finally, Panel D reports descriptive statistics according to whether firms decide to restart previously abandoned NPD projects and whether they are credit-constrained. Approximately 138% (i.e., 714 firms) are NPD-restart firms, of which approximately 42% (301 out of 714) are credit constrained firms, whereas 53% of NPD non-restarts are credit constrained, suggesting that a higher share of NPD restarts is financially unconstrained. This preliminary descriptive statistic suggests a negative correlation between credit constraints and the probability of restarting NPD innovation projects. Finally, Panel D of Table 1 presents the t-statistics for the mean difference between firms, whether to restart previously abandoned or suspended NPDs when the sample is split between credit constrained and other firms. On average, 15.2% of credit-unconstrained firms are likely to restart NPDs, whereas this ratio is 13.7% for credit-constrained firms. The mean difference between the two groups of firms was also statistically significant using the t-test of mean differences. In other words, credit-unconstrained firms are approximately 10.95% more likely to restart previously abandoned or suspended NPDs than are credit-constrained firms. These preliminary univariate tests warrant detailed econometric investigations to establish causal relationships between credit constraints and firms’ innovation propensity for NPD restarts. This result is also in line with that of Sasidharan et al. (2015), who found a limited role for debt financing in R&D investments for Indian manufacturing firms.

EMPIRICAL RESULTS

Financing constraints and innovation propensity for previously abandoned NPD

Table 2 presents the estimated coefficients and marginal probabilities of the estimations for bivariate probit models. Firm vectors, industry dummies, and country fixed effects are included in all regressions. As presented in Table 2, the correlation coefficient between the error terms of the two models, rho, is statistically significant for all models, indicating the appropriateness of the bivariate probit models for our empirical estimations.

Table 2. Credit constraints and restarting previously suspended NPD

|

|

(1) |

(2) |

(3) |

(4) |

(5) |

|

VARIABLES |

Credit constraint |

Marginal effects |

High-Tech sector dummy |

Interaction terms |

Interaction terms |

|

FC |

-1.549*** |

-0.235*** |

-1.435*** |

-1.346*** |

-1.148*** |

|

(0.0612) |

(0.0045) |

(0.271) |

(0.184) |

(0.112) |

|

|

SMALL_FIRM |

0.0755* |

0.025 |

0.060 |

0.0550 |

0.056*** |

|

(0.0444) |

(0.0197) |

(0.0524) |

(0.0460) |

(0.0123) |

|

|

MEDIUM_FIRM |

0.155** |

0.043** |

0.140* |

0.139** |

0.144*** |

|

(0.0606) |

(0.0186) |

(0.0747) |

(0.0708) |

(0.0361) |

|

|

HIGH_TECH |

0.0632* |

0.140** |

|||

|

(0.0341) |

(0.0548) |

||||

|

-0.188* |

|||||

|

(0.103) |

|||||

|

-0.328*** |

|||||

|

(0.121) |

|||||

|

Group affiliation |

-0.147*** |

-0.0141* |

-0.188** |

-0.187*** |

-0.159*** |

|

(0.0446) |

(0.0079) |

(0.0786) |

(0.0701) |

(0.0303) |

|

|

MOI |

-0.014** |

-0.0148** |

-0.102* |

-0.106** |

-0.106*** |

|

(0.0429) |

(0.00318) |

(0.0585) |

(0.0536) |

(0.0338) |

|

|

AGE |

-0.0718** |

-0.019** |

-0.0605 |

-0.0620 |

-0.0635** |

|

(0.0346) |

(0.0070) |

(0.0422) |

(0.0392) |

(0.0264) |

|

|

EXPORTER |

-0.102** |

-0.015** |

-0.0875*** |

-0.0854*** |

-0.117 |

|

(0.0507) |

(0.0068) |

(0.0269) |

(0.0297) |

(0.0790) |

|

|

TRGI |

-0.194*** |

-0.029** |

-0.202*** |

-0.201*** |

-0.203*** |

|

(0.0513) |

(0.0090) |

(0.0566) |

(0.0519) |

(0.0442) |

|

|

GNFIN |

0.134*** |

0.020*** |

0.138** |

0.138** |

0.151*** |

|

(0.0413) |

(0.0073) |

(0.0603) |

(0.0551) |

(0.0197) |

|

|

APPLY_PATENT |

0.169*** |

0.025*** |

0.189*** |

0.193*** |

0.180*** |

|

(0.0228) |

(0.0022) |

(0.00769) |

(0.0141) |

(0.0420) |

|

|

COUNTRY dummy (BANGLADESH) |

-0.536*** |

-0.118*** |

-0.543*** |

-0.534*** |

-0.147** |

|

(0.0538) |

(0.0131) |

(0.0446) |

(0.0439) |

(0.0626) |

|

|

COUNTRY dummy (PAKISTAN) |

-0.760*** |

-0.151*** |

-0.729*** |

-0.721*** |

|

|

(0.0481) |

(0.0068) |

(0.07296) |

(0.0679) |

||

|

COUNTRY_INDIA |

0.817*** |

||||

|

(0.146) |

|||||

|

Constant |

-0.789*** |

0.173 |

0.146 |

-0.970*** |

|

|

(0.171) |

(0.278) |

(0.227) |

(0.120) |

||

|

Rho |

1.464*** |

1.216* |

1.231** |

1.197*** |

|

|

Wald test of rho=0 |

16.58*** |

3.239* |

4.381** |

110.31*** |

|

|

Observations |

3,560 |

3,552 |

3,560 |

3,560 |

3,560 |

|

Country & industry Dummies |

YES |

YES |

YES |

YES |

YES |

Note: Second stage regression results of the bivariate probit model (standard error in parenthesis, clustered at the country-level). Key explanatory varaible for each model is mentioned at the top of each column. The dependent variable for all regressions is PABAN, a dummy variable for whether a firm initiates previously abandoned innovation project for NPD, 0 otherwise. FC is a measure of credit constraint as defined in the Variable measurements section.

This specification served as the base model. The regression specification in Column 1 tests the impact of credit constraints (FC) on the likelihood of restarting previously suspended innovation projects for NPD after controlling for firm and innovation vectors and industry and country fixed effects. The results for the firm vectors show that the coefficient estimates for firm size and age suggest that smaller and younger firms are more likely to restart previously abandoned NPDs, consistent with the idea that young firms are more agile by engaging in riskier innovations to catch up with larger and established firms. However, the small magnitude and statistical significance of the marginal probabilities (column 2) suggest that size and age are less significant for firms’ innovation propensity to restart abandoned/suspended NPDs. Multi-establishment and export-oriented firms are less likely to restart their NPDs. Again, the magnitude of the marginal probabilities (Column 2) for the two variables suggests that export and multi-establishment status may have less of an impact on a firm’s innovation propensity for an NPD restart. This result casts doubt on the general findings of previous studies on the existence of internal capital markets and the positive spillover effects of R&D and resource sharing within business groups. For instance, recent studies suggest that group affiliation and the associated internal capital markets may not guarantee insurance against a firm’s financial constraints or access to external financing (e.g., Bhaumik, Das, & Kumbhakar, 2012). George, Kabir, and Qian (2011) report similar results for capital investments in group-affiliated firms in India. Our result is also in line with that of Sasidharan et al. (2015), who found marginal differences between cash flow sensitivity and R&D investments between group-affiliated and stand-alone Indian firms.

However, innovative firms (i.e., those that apply for patents) and firms that receive government support for innovation are more likely to restart previously abandoned or suspended NPDs. Innovation propensity and government subsidies are positively and statistically significantly related to the probability of a firm restarting previously suspended or abandoned NPDs. The impact of these two variables is much greater than that of the other firm and innovation vectors, as shown by the comparatively higher magnitude and statistical significance of their coefficient estimates at the 99% confidence level.

The probability of NPD restarts is significantly affected by cross-country differences. Using India as the reference category, the coefficients for the country dummies for Pakistan and Bangladesh are negative and highly statistically significant (at the 99% level), indicating a higher likelihood of firms restarting NPDs in India than in Pakistan or Bangladesh. In other words, firms in India are more likely to restart NPDs than firms in Pakistan and Bangladesh. The largest difference in innovation propensity for NPD restarts is for firms located in Pakistan and India, which represents the mean difference between Indian and Pakistani firms. This finding is supported by the higher magnitude of the marginal effect of the coefficient (Column 2), which indicates that Indian firms are approximately 15% more likely to restart previously abandoned NPDs than firms in Pakistan, ceteris paribus. The coefficients for country dummies suggest that country differences is an important factor in explaining differences in innovation propensity in NPD restarts. This result is not surprising given that Indian firms have increasingly focused on global competitiveness through increased R&D spendings and innovation (Sasidharan et al., 2015) compared to other South Asian economies.

FC is a measure of credit constraints and is the key explanatory variable. Column 1 of Table 2 shows that the coefficient estimate for FC is negative and statistically significant at the 99% confidence level, suggesting that credit constraints negatively affect the probability of a firm restarting previously suspended (or abandoned) NPDs. Furthermore, the marginal probability for credit-constrained firms evaluated at the sample mean, as reported in Column 2, indicates that the probability of restarting NPDs increases significantly and statistically by 23.5% in the absence of credit constraints, which is a substantial increase in the incidence of NPD restarts. Recent empirical studies suggest that binding financing constraints increase the likelihood of innovation project failure (García-Quevedo et al., 2018). Consequently, some innovation projects have not been restarted or delayed, because of a lack of adequate financial resources. This result is also in line with Mohnen et al. (2008), who found a positive relationship between binding financing constraints and the probability of NPDs not starting an innovation project for Netherland firms using the CIS 3.5 innovation survey. Similarly, Canepa and Stoneman (2003), show that financial obstacles are more important than other endogenous and exogenous obstacles in their impact on the probability of “not starting, delaying, or postponing” innovation projects in European countries. In short, our empirical results are consistent with studies from developed countries and literature on financial obstacles to innovation (Khan & Rizwan, 2020; Mancusi & Vezzulli, 2014; Savignac, 2008). Empirical literature shows that obstacles to innovation may be related to a lack of finance and cost factors (D’Este, Iammarino, Savona, & Von Tunzelmann, 2012). Although technically and economically viable, they may be suspended (or put on hold) because other rewarding projects that require the same resources are available. A suspended (or abandoned) NPD project can be restarted when a firm’s resource constraints are resolved.

In Column 3 of Table 2, industry dummies are replaced with an indicator variable, HIGH-TECH, that equals one for firms in the high-technology innovation intensive sectors, namely chemicals, electronics and communications, engineering, rubber and plastics, information technology and related services. This variable was included in the regression to explore innovation propensity across high-tech and low-tech sectors. The coefficient estimate of the variable is positively and statistically significantly related to the firm’s innovation propesnity for NPD restarts. As expected, firms in innovation-intensive industries are more likely than low-tech sectors to restart NPDs. An interaction term between a measure of credit constraint and the indicator variable for high-tech sectors, denoted by, was included in regression, as reported in Column 4 of Table 2, to explore the differential impact of credit constraints on the likelihood of restarting NPDs accross high-technology and low-technology sectors. The negative coefficient of the credit constraint dummy variable indicates that constrained firms in low-tech sectors are less likely than unconstrained firms to restart previously suspended NPD. In other words, unconstrained firms in low-tech sectors are more likely to restart NPD and constrained low-tech firms are less likely to restart NPD. Furthermore, the positive coefficient for indicates that credit-unconstrained firms are more likely to restart previously abandoned (or suspended) NPD than credit-constrained firms in high-tech sectors are. In summary, the negative and positive coefficients of FC and HIGH-TECH suggest that credit-constrained firms, whether in the high-tech or low-tech sectors, are less likely to restart abandoned/suspended NPDs. This was confirmed by the negative coefficient of the interaction term between FC and HIGH-TECH.

In column 5, Table 2, we introduce the interaction term of the variable FC with the variable COUNTRY_INDIA. We include this interaction term to test whether the effect of credit constraints on the firm’s propensity to restart NPDs depends on the country-level fixed effects (the country dummy captures the country differences in the level of development of institutions, regulatory environment and financial and economic development). The positive and statistically significant coefficient for COUNTRY_INDIA suggests that credit-unconstrained Indian firms are more likely to restart NPDs than credit-unconstrained firms in Pakistan and Bangladesh, indicating a higher innovation propensity for firms in India. This finding supports the earlier results in Table 2 that Indian firms are more likely to restart NPDs than firms in the other two countries in our sample. However, the coefficient of the interaction term is negative and statistically different from zero at the 95% confidence level, suggesting that credit-constrained firms in India are less likely to restart NPDs than are similar firms in Pakistan and Bangladesh. This finding suggests that the effect of credit constraints is more severe in Indian firms than in Pakistani or Bangladeshi firms. This result is unsurprising given that Indian firms have better access to external finance, where financial markets in India are more efficient and developed than those in Pakistan and Bangladesh. Better developed capital markets in India are more efficient at allocating financial resources to more productive investments.

Next, we consider the type of finance used to fund innovation in order to explore whether it affects a firm’s propensity to restart NPDs. Various forms of financing exhibit varying degrees of characteristics in terms of maturity, formality, and risk (Girma & Vencappa, 2015; Rizwan & Khan, 2007; Khan & Hijazi, 2009), indicating that various sources of finance may have differential inmpact on the firm’s propensity to restart NPDs. We compare innovations funded by banks to those funded by internal funds to examine whether different sources of financing have a heterogenous impact on a firm’s decision to undertake previously abandoned (or suspended) NPDs. We have data from the IFS surveys on how technological innovation (i.e., product and service innovations). The main funding sources were internal funds, bank loans, government agencies and departments, Non-Governmental Organizations, and international organizations. Many firms used multiple sources of financing to fund their NPDs. The funding sources were measured using binary variables. We constructed three dummy variables for whether a firm uses only bank finance (denoted by ONLY_BANK), internal funds (denoted by ONLY_OWN), or whether a firm used both sources of finance (denoted by OWN_BANK) to fund innovation investments.

Since the bank’s acceptance of the firm’s loan requests is not a randomized event, we control for sample selection bias in a two-step bivariate probit model. The dependent variable is also binary (restarting of NPD). In this situation, seemingly unrelated (SUR) binary probit regression is appropriate for our econometric specification. The same variables that we employed as instruments for credit constraint indicators were used as instruments for the probability that a firm funds innovation activities through bank loans. Columns (3) to (5) of Table 3 report the results of the second-stage bivariate probit model. Our main variables of concern are the measures of bank financing, internal funds, and a combination of both internal funds and bank finance.

Table 3. Extramural R&D, Credit constraints, and NPD

|

(1) Extramural R&D |

(2) Interaction of FC & Extramural R&D |

(3) Internal Funding of innovation |

(4) Bank Funding of innovation |

(5) Internal & Bank funding of innovation |

|

|

FC |

-1.545*** |

-1.538*** |

|||

|

(0.0395) |

(0.0808) |

||||

|

EXTRAM_RND |

0.194*** |

||||

|

(0.0465) |

|||||

|

ONLY_OWN |

0.505*** |

||||

|

(0.161) |

|||||

|

ONLY_BANK |

-1.430*** |

||||

|

(0.2610) |

|||||

|

OWN_BANK |

-0.632** |

||||

|

(0.284) |

|||||

|

EXTERAM_RND*FC |

0.117** |

||||

|

(0.0530) |

|||||

|

SIZE |

-0.0297*** |

-0.0244*** |

0.182*** |

0.039** |

0.107*** |

|

(0.00476) |

(0.00762) |

(0.0278) |

(0.0149) |

(0.0128) |

|

|

Group Affiliation |

-0.143*** |

-0.156*** |

-0.199*** |

-0.227*** |

-0.234*** |

|

(0.0323) |

(0.0449) |

(0.0692) |

(0.0453) |

(0.0715) |

|

|

MOI |

-0.0920** |

-0.0990** |

-0.250*** |

-0.090 |

-0.178*** |

|

(0.0405) |

(0.0468) |

(0.0468) |

(0.0645) |

(0.00927) |

|

|

AGE |

-0.0691** |

-0.0697* |

0.0290 |

0.033 |

0.0135 |

|

(0.0349) |

(0.0361) |

(0.0268) |

(0.0437) |

(0.0175) |

|

|

TRGI |

-0.208*** |

-0.201*** |

-0.416*** |

-0.253*** |

-0.282*** |

|

(0.0482) |

(0.0535) |

(0.0183) |

(0.0458) |

(0.0262) |

|

|

GNFN |

0.133*** |

0.136*** |

-0.00541 |

0.1777*** |

-0.0538*** |

|

(0.0452) |

(0.0482) |

(0.00352) |

(0.0241) |

(0.00641) |

|

|

APPLY_PATENT |

0.159*** |

0.172*** |

0.176*** |

0.221*** |

0.00519 |

|

(0.0312) |

(0.0234) |

(0.0177) |

(0.0447) |

(0.0502) |

|

|

COOP |

-0.156** |

-0.143** |

-0.350*** |

-0.125* |

-0.295*** |

|

(0.0616) |

(0.0611) |

(0.0106) |

(0.0674) |

(0.0525) |

|

|

Constant |

-0.650*** |

-0.674*** |

-1.417*** |

-1.337*** |

-1.021*** |

|

(0.203) |

(0.257) |

(0.289) |

(0.153) |

(0.0503) |

|

|

Marginal Effects (FC, ONLY_OWN, ONLY_BANK) |

-0.153** |

0.036** |

-0.016** |

||

|

Marginal Effects (EXTRAM_RND*FC) |

0.0117* |

||||

|

Rho |

1.508*** |

1.443*** |

-0.390*** |

0.713** |

0.525** |

|

Wald test of rho=0 |

31.09*** |

14.79*** |

36.77*** |

15.52*** |

5.93** |

|

Observations |

3,533 |

3,533 |

981 |

3,604 |

2,075 |

|

Country & Industry dummies |

YES |

YES |

YES |

YES |

YES |

Note: Second stage regression results of the bivariate probit model (standard error in parenthesis). Key explanatory varaible for each model is mentioned at the top of each column. The dependent variable for all regressions is PABAN, a dummy variable for whether a firm initiates previously abandoned innovation project for NPD, 0 otherwise. FC is a measure of credit constraint as defined in theVariable measurements section. In Column 2, EXTRAM_RND is a dummy variable for whether a firm has collaborative R&D arrangements with external partners. Column 3 consists of an interaction term between EXTRAM_RND and FC. ONLY_OWN, ONLY_BANK, and OWN_BANK are dummy variables for whether a firm funds innovation with only internal sources, bank finance, or both bank funding and internally generated funds, respectively. The significance levels for each coefficient are represented by asterisks: *** = 1%; ** = 5%.

The positive and statistically significant coefficient of internal funds (ONLY_OWN) in Column 3 indicates that firms with sufficient internal funds are more likely to initiate previously abandoned innovation activities for NPD. By contrast, firms that employ only bank credit to fund innovation investments are less likely to undertake previously abandoned R&D projects as the coefficient of ONLY_BANK is negatively statistically significantly related to the likelihood of restarting previuosly abandoned or suspended NPDs. This result is consistent with the view that internal funds are more important for innovation activities than costly external finance is, particularly debt financing in developing countries (Brown, Martinsson & Petersen, 2012). This result is also consistent with our expectation that firms in South Asia rely more on internal financing to fund innovation, whereas traditional financing sources, such as banks and financial institutions, play a limited role despite significant developments in the financial sector of countries like India. The same factor is captured in the variable that considers both internal and bank financing for funding NPD innovation projects, as indicated by the negative coefficient of OWN_BANK. Our results are consistent with those of Sasidharan et al. (2015) for Indian firms, who found that internally generated funds are the preferred source of R&D financing, whereas external financing, both equity and debt, are not significantly related to R&D investments. They also attribute their findings to the excessively low ratio of new stock issuance to total assets by Indian firms, which was 0.018, which is very low compared to that of U.S. firms (0.204), as reported by Brown, Fazzari and Petersen (2009), and European firms (0.108), as reported by Brown et al. (2012).

Extramural R&D and innovation project initiation

We also explore whether extramural R&D attenuates the relationship between financial obstacles and the likelihood of restarting previously abandoned (or suspended) NPD projects. Several firms in our dataset have adopted both internal and extramural R&D for innovative product development. The IFS survey defines extramural R&D as “creative work, undertaken by other enterprises, public or private research organizations, which was paid for by this establishment.” Therefore, if a firm had undertook external R&D, we define a dummy variable, EXTRAM_RND. Column 1 of Table 3 presents the results of the bivariate probit model where EXTRAM_RND was included in the regression from Column 1. Extramural R&D positively and statistically significantly increases the probability of a firm undertaking previously abandoned (or suspended) NPD. This result is consistent with our theoretical prediction that firms with extramural R&D have an increased likelihood of reinitiating previously abandoned/suspended NPD innovation projects. Firms with collaborative R&D strategies exploit complementary expertise and resources and build their capacity to enhance innovation efficiency and productivity (Mowery, Oxley, & Silverman, 1998).

To capture the effect of credit constraints in the presence of extramural R&D, we include the interaction of FC with the measure for extramural R&D (EXTRAM_RND × FC). This interaction term was included in a separate model. The positive and statistically different from zero coefficient of the interaction term (Column 2 of Table 3) suggests that credit constraints are less binding for firms with collaborative R&D investments. Extramural R&D may reduce the reliance of financially constrained firms on their own resource requirements, thereby enhancing innovation efficiency and productivity (Mowery et al., 1998). Furthermore, an extramural R&D attenuates a firm’s financing constraints and increases its access to external financing.

Collaboration breadth and NPD restarts

The independent variable chosen to test Hypotheses 2a and 2b is measured using the channels through which a firm formally collaborated to develop innovative products and services. Following Laursen and Salter (2006), we construct R&D collaboration breadth, denoted by COLB_BRDTH, as the sum of the number of cooperating partners for NPD, where each source is assigned a value of one if a firm has collaborated with the specific channel in question. These collaborating partners, as reported by the IFS survey, include “domestic firms, foreign firms (or foreign-owned parent firms), domestic or foreign academic institutes, research organizations, private consulting companies or individuals, and government agencies.” Simply put, for each firm, the index takes a value between zero (non-collaborating firms) and six. Therefore, the breadth of a firm’s collaboration increases its index value.

We use an instrumental variable approach because several factors affect both the probability of a firm collaborating with one or more partners based on their needs and capabilities and the probability that a firm decides to commit resources to restart previously abandoned innovation projects for NPD (Medda, 2018). For instance, larger firms are more likely to have several inter-organizational collaborations and are likely to have few R&D project abandonments because they may be simultaneously involved in several innovation projects and activities. As our dependent variable, PABAN, is an indicator variable, we employed a probit model with a continuous endogenous regressor (Stata command: ivprobit) to account for the potential endogeneity between the breadth of collaboration types and PABAN. Following Czarnitzki and Hottenrott (2017), the instruments employed for collaboration breadth are (a) the share of R&D performers in a firm’s industry (2-digit ISIC Code 3.1) and (b) the share of firms with extramural R&D in the firm’s industry. The appropriateness of the exclusion restriction was tested using auxiliary regression in which the dependent variable was PABAN. The coefficient estimates for both variables were statistically insignificant.

Column 1 (first-stage regression) and Column 2 (second-stage regression) of Table 4 reports the results of the probit model with endogenous regressors (Stata command: ivprobit).

Table 4. Collaboration breadth and Innovation

|

|

(3) |

(4) |

(5) |

||

|

(1) Collaboration Breadth (1) (2) |

Industry-related Collaboration Breadth |

Academia-related Collaboration Breadth |

Financial constraint |

||

|

|

Stage 1 |

Stage 2 |

|

|

|

|

FIN_MAJOR |

-1.639*** |

||||

|

(0.1052) |

|||||

|

COLB_INDUSTRY |

-2.366*** |

-0.294 |

|||

|

(0.512) |

(0.242) |

||||

|

COLB_ACADMIC |

-2.464*** |

||||

|

(0.1795) |

|||||

|

COLB_BRDTH |

-1.606*** |

||||

|

(0.3534) |

|||||

|

SIZE |

-0.0354*** |

-0.0152 |

0.068 |

-0.0835 |

-0.028*** |

|

(0.00499) |

(0.0373) |

(0.0996) |

(0.0839) |

(0.00693) |

|

|

R&D INTENSITY |

-3.4e-08*** |

-3.70e-07* |

-4.44e-07 |

-7.19e-08 |

-0.0019 |

|

(5.91e-11) |

(2.07e-07) |

(8.08e-07) |

(1.28e-07) |

(0.00130) |

|

|

Group Affiliation |

0.146*** |

0.189 |

0.156 |

0.139 |

-0.067** |

|

(0.00224) |

(0.141) |

(0.334) |

(0.263) |

(0.0307) |

|

|

MOI |

0.0262*** |

-0.125* |

0.184 |

-0.173 |

-0.173*** |

|

(0.00807) |

(0.0730) |

(0.455) |

(0.238) |

(0.0138) |

|

|

AGE |

0.108* |

0.0814 |

-0.00814 |

0.143 |

-0.028 |

|

(0.0637) |

(0.207) |

(0.202) |

(0.139) |

(0.0241) |

|

|

EXPORTER |

0.156*** |

0.366*** |

-0.122 |

0.449* |

-0.0129 |

|

(0.00660) |

(0.00272) |

(0.297) |

(0.254) |

(0.0197) |

|

|

TRGI |

0.262*** |

0.565*** |

0.708*** |

0.246 |

-0.185*** |

|

(0.0537) |

(0.0922) |

(0.249) |

(0.213) |

(0.0198) |

|

|

APPROPRIABILITY |

0.141*** |

0.176 |

0.0764 |

0.251*** |

1.304*** |

|

(0.0458) |

(0.216) |

(0.151) |

(0.0863) |

(0.1540) |

|

|

APPLY_PATENT |

0.1998323 |

0.1718908 |

0.095 |

0.282 |

-0.0284 |

|

(0.2955) |

(0.1573) |

(0.4223) |

(0.34710 |

(0.0368) |

|

|

Exclusion Restriction 1: Share of R&D performers (industry) |

0.491 |

||||

|

(0.322) |

|||||

|

Exclusion Restriction 2: Share of R&D collaborators (industry) |

-0.408*** |

||||

|

(0.118) |

|||||

|

GNFIN |

-0.0187 |

||||

|

(0.0187) |

|||||

|

GOVT_SUPORT |

0.548*** |

-0.187*** |

|||

|

(0.0263) |

(0.00778) |

||||

|

Constant |

0.303*** |

122 |

0.549 |

0.349 |

-0.198*** |

|

(0.0434) |

(0.109) |

(0.619) |

(0.513) |

(0.0525) |

|

|

Wald chi2(3) |

179484.22*** |

78.29** |

240.92*** |

||

|

Log Likelihood |

-135.328 |

-79.19 |

-115.11 |

-1556.20 |

|

|

Rho |

2.202*** |

1.89** |

1.90** |

||

|

Wald test of exogeneity: chi2(1) |

9.82*** |

6.28** |

2.86** |

||

|

Wald test of rho=0 |

6.65*** |

||||

|

Observations |

122 |

122 |

116 |

121 |

2,005 |

|

Country Dummies |

YES |

YES |

YES |

YES |

YES |

Note: Instrumental variable probit model coefficients (standard error in parenthesis, clustered at the country level) for columns 1 – 4. Stage-1 and stage-2 regression estimations in Columns 1 – 2 contain a constant, country, and industry fixed effects. The dependent variable for all models, PABAN, is a dummy for whether a firm restarts the prior innovation projects for NPD that were suspended/abandoned before completion. The key independent variable is mentioned at the top of each column. COLB_BRDTH is a sum of dummy variables for whether a firm has collaborated with the particular type of collaborating partner for NPD. COLB_BRDTH thus can assume a value between 0 (no collaboration) to a maximum of 6 (a firm collaborated with all partners as reported in the IFS survey). Column 5 presents second-stage results of the Seemingly Unrelated bivariate Probit model. FIN_MAJOR is a self-reported, perceived measure of financial constraints. COLB_INDUSTRY and COLB_ACADMIC are dummy variables for whether a firm has R&D collaboration with industry (foreign or domestic firm or a government agency) or academia (foreign or domestic research institute, a consultancy firm or an individual), respectively. The operational definitions of other variables are as reported in the Methodology section. The significance levels for each coefficient are represented by asterisks: *** = 1%; ** = 5%.

The Wald test of the exogeneity, reported in Column 1, rejects the null hypothesis of no endogeneity and confirms the appropriateness of the specification for modeling the relationship between innovation propensity and extramural R&D breadth. The coefficient estimate of our main variable of concern, COLB_BRDTH, is negative and statistically significant at the 1% level of significance. This negative coefficient, consistent with Hypothesis 2b, suggests that a higher breadth of inter-organizational collaborations decreases the probability that a firm restarts previously suspended (or abandoned) NPDs. Although R&D alliances enhance innovation efficiency and productivity for the focal firm (e.g., Hu, McNamara & Piaskowska, 2016; Medda, 2018), several studies show that these alliances are fraught with problems and increased costs because of the managerial and technical complexities arising from collaborating with various R&D collaborating partners. In other words, a wide-ranging external knowledge search involves high marginal costs owing to the greater complexity of knowledge management and the relationships necessary to maintain access to these resources (Leiponen & Helfat, 2010).

Robustness checks

First, we consider an alternative financing constraint indicator. We consider a firm’s limited access to credit as a measure of financial obstacles, conveniently overlooking the fact that financing constraints also encompass difficulties in accessing all sources of financing (Brown et al., 2012). As in Khan, Shah and Rizwan (2021), we construct a measure of financial obstacles generated from the response item “k30” of enterprise surveys that asks managers how they perceive access to finance as an obstacle on a 5-point Likert scale. The variable FIN_MAJOR takes the value of 1 if a manager perceives finance access as either “a major or very severe obstacle; otherwise, it equals zero for response items “no obstacle, minor obstacle, or moderate obstacle”. This self-report measure captures the degree of perceived difficulty in accessing external finance, and has been shown to be informative in identifying firms constrained in their access to finance (e.g., Caggese & Cuñat, 2008). The econometric procedure and instrumental variables used to model FC were also employed in the regression specification for this measure of financing constraints. Table 4 (Column 5) presents the results of the bivariate probit model. The negative and statistically significant coefficient estimates for FIN_MAJOR indicate that the empirical results are consistent with those shown in Table 2. Financial constraints are likely to reduce the probability that a firm will restart or attempt to start innovation projects for suspended (or abandoned) NPDs.

Prior research employed search breadth by including all sources of external knowledge in a single measurement of collaboration breadth. Different sources of knowledge require varying processes, institutional norms, cultures, and contracts (Antolin-Lopez, Martinez-del-Rio & Cespedes-Lorente, 2015). Consequently, we distinguish between a firm’s collaboration with industry from the firm’s collaborations with academia. As in Wu (2014), we decomposed the overall search breadth into (a) industry-related search breadth and (b) academia-related search breadth. The former was computed with a dummy variable using the firm’s R&D collaborations with “domestic firms, foreign firms or a foreign-owned parent firm” while the later was computed as a dummy variable using the firm’s collaborations with “domestic and (or) foreign academic or research institutions, private consultants, or individuals.” Columns 3 – 4 of Table 4 report the empirical results of the instrumental variable probit model. The negative and statistically significant coefficient estimates for both measures of breadth in knowledge sourcing confirm the earlier results of the negative impact on the probability of restarting previously suspended/abandoned NPD innovation projects.

CONCLUSION

This study examines the effect of financial constraints on a firm’s decision to restart (or attempt to restart) the previously abandoned or suspended innovation projects for NPD. In recent years, a growing stream of studies on financial obstacles to innovation tends to support the evidence of an increase in the risk of innovation project failures, delays, or abandonment for firms facing binding financing constraints. We contribute to the literature by examining the importance of financial obstacles in the probability that a firm decides to undertake innovation projects for NPDs that were previously suspended (or abandoned). Controlling for the endogeneity between innovation propensity and financial constraints, we show that credit constraints significantly reduce the probability that a firm undertakes previously abandoned/suspended NPDs. These results support the general view that financial obstacles to innovation negatively affect the innovation propensity. We further show that an extramural R&D attenuates the relationship between credit constraints and the firm’s propensity to start previously abandoned NPDs, which is consistent with our theoretical prediction that an extramural R&D attenuates a firm’s credit constraints and enhances innovation propensity.

While our findings support the notion that extramural R&D attenuates credit constraints, which in turn increases the likelihood of restarting previously abandoned or suspended NPDs, we did not find that R&D collaboration breadth (i.e., the number of various types of collaborating partners) positively influences the probability of a firm undertaking prior innovation projects for NPD. These results support the notion that the probability of a firm undertaking NPD innovation projects is lower for those collaborating with a wide range of partners. This result generally supports the Optimal Combination of R&D Hypothesis, which states that a firm must maintain a balance between internal R&D and extramural R&D to optimize innovation performance. While the cost factors and “managerial attention constraints” could be potential explanations, further research is needed to identify specific reasons.

Furthermore, significant cross-country differences in firm-level innovation propensity were found among firms. Specifically, firms in India are more likely to restart NPDs than firms in Pakistan and Bangladesh, which is consistent with recent literature suggesting India’s significant progress in R&D spending and technological progress compared to its neighboring countries in South Asia. India has invested massively in transforming itself into a knowledge economy and private firms have shown increased innovation performance (Zhang et al., 2016). However, credit-constrained firms in India are less likely to restart NPDs than firms in Pakistan and Bangladesh. This finding suggests that the effect of credit constraints is more severe for Indian firms than it is for firms in other South Asian countries. This result is unsurprising given that financial markets in India are more developed and efficient at allocating financial resources to more productive investments compared to other developing countries. Industry-level empirical analysis shows that credit-constrained firms, whether in high- or low-tech sectors, are less likely to restart abandoned (or suspended) NPDs. Furthermore, we observe a strong preference for internal funds for NPD financing in South Asian countries, whereas external financing, particularly bank credit, plays a limited role in NPD financing, consistent with recent studies of developing markets.